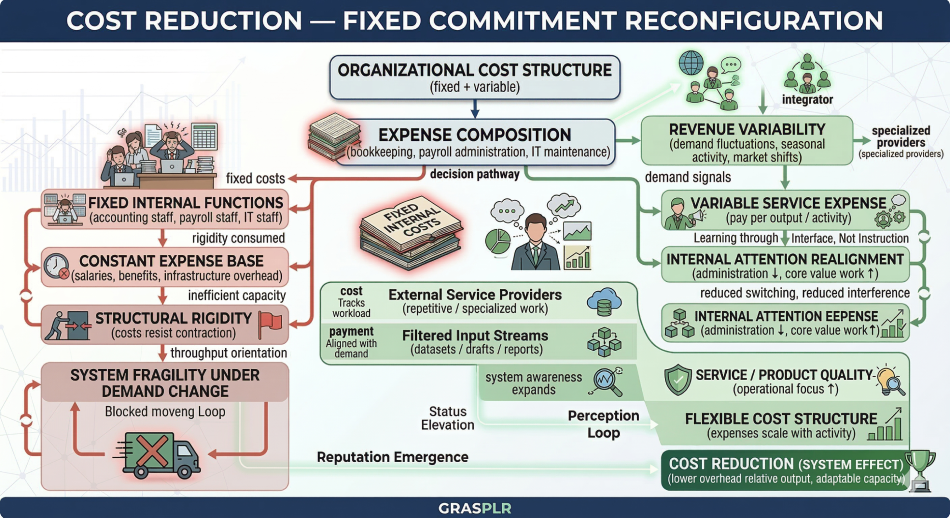

Cost reduction is often framed as a matter of restraint: spending less, cutting back, tightening control. Yet when organizations successfully reduce costs without degrading performance, the change usually comes from reconfiguration rather than reduction.

A familiar example is a small restaurant facing competitive pressure. Margins are thin, demand fluctuates, and many expenses are fixed regardless of how busy the dining room is. Bookkeeping and accounting must be done whether revenue is high or low, but hiring a full-time specialist permanently adds salary, benefits, software licenses, and workspace to the cost base.

Outsourcing shifts this structure.

Instead of carrying accounting as a fixed internal function, the restaurant converts it into a variable service. Costs begin to track actual activity rather than anticipated need. This adjustment alone alters the financial dynamics of the system.

Fixed Costs as Structural Rigidity

In systems terms, fixed costs increase rigidity. They reduce an organization’s ability to adapt to variation in demand because expenses remain constant even when revenue does not.

Decision-making becomes less about protecting sunk costs and more about responding to current conditions. In this environment, financial goals are easier to meet because the system resists less.

Cost reduction, then, is not just a financial outcome. It is a structural one, arising from how commitments are designed and distributed.